Have you properly prepared your succession plan? Did you cover all the bases? Passing the torch to the person who will take over your business is no easy feat.

This transferor’s testimonial reminds us of the importance of having a well-planned succession plan and making sure all the bases are covered.

Sound management, communication and openness to the needs and objectives of all those involved are factors to be taken into consideration when carrying out a business transfer and, for parties concerned, ensuring that the business goes on.

Expect the transfer to take several years

Régis Simard founded Les Forestiers F.A.J. inc. in 1995. His wife, Johanne, is also involved in the company, as secretary-accountant. For several years, they had been thinking of selling the company.

“I didn’t want just anybody to take over the business,” explains Régis. “Keeping it going is important. I’d been talking about this to Jean-Louis for about four or five years. He’s been a key employee for 18 years and is married to my niece.”

An automobile accident at the age of 57 led Régis to initiate the transfer process, which sped things up.

According to the Simards, Jean-Louis has always been a good candidate for succession. He’s resourceful, bold and versatile and he likes the forest. They believe these are essential qualities for the job. To be an owner, you also have to be dedicated. The work is demanding, sometimes you have to be away for several days, and you can be called at any time, day or night.

“These days, work is important, but family and leisure time are just as much. That’s why taking over a business is a decision that has to be made as a couple.”

A succession plan to manage expectations

“The transfer is going well,” Régis maintains. “There are ups and downs. The successor has expectations and, as transferor, I had some as well. With good communication, we can find common ground. This is not the same as a sale. You want the successor to be able to keep the business.”

“Everything is going smoothly,” says Johanne. “There are considerable challenges in this transfer, the successor is our nephew-in-law, we wanted it to go well. Having an external consultant as intermediary to coordinate everything helped. We wanted a win-win for everyone.”

Régis goes on to say, “There are hundreds of ways to transfer a business. For us, it was important that Jean-Louis not be financially overwhelmed, otherwise he wouldn’t have been able to continue. We needed sound management and the support of experienced people to find the best plan to ensure the company’s longevity.”

For the future, Régis Simard would like to see the company maintain its industry position while continuing to offer the same quality and expertise that characterized it from the onset.

You could also like to read

Next article

The customer experience is a hot topic. However, more than simply being a buzzword, it’s an essential business strategy component that can no longer be pushed to the back burner or ignored.

Focussing on the customer experience can in fact help you:

- Protect your income by fostering loyal customers;

- Cut the costs associated with customer attrition and acquisition rates;

- Improve the efficiency and effectiveness of your tools, processes and Customer “channels”;

- Engage your employees thanks to a customer-focussed culture;

- Foster greater productivity and decrease staff turnover;

- Stand out from the competition – while copycat risks increase and margins decrease, the customer experience is a differentiating factor.

The customer experience is the result of all the interactions a customer can have with regard to a brand or business, or what the customer has seen and felt. It’s the art of making a positive, long-lasting impression.

Talking about the customer experience emphasizes the rational and emotional benefits underlying the purchase of a service or product rather than simply its characteristics. Therefore, it’s the customer’s perception that counts; you need to modify it to ensure the customer has a positive experience.

Let’s be honest: how well do you really know your customers? What kind of customer experience are you trying to provide? Which emotions are you trying to evoke? What are your customers really looking for? What creates value for your organization? And especially, how focussed is your organization on its clientele?

More loyal customers, enhanced reputation

It’s no longer enough to simply satisfy your customers. You need to make them loyal and encourage them to recommend you so that your organization can reap tangible benefits. Why is this important?

- Recruiting a new customer costs five times more than retaining an existing one (TARP Institute – USA).

- A dissatisfied customer will tell about 13 people on average, but only 1 out of 25 will actually contact you to complain;

- A satisfied customer will tell five people;

- On average, customer experience leaders achieve greater stock market returns regardless of economic cycles, according to a post entitled Is there a Return on Customer Experience Investments? published on the Watermark Consulting blog.

Where to begin?

With customers of course! First and foremost, is knowing your customers well and having a clear idea of the customer experience you wish to offer.

Make sure to know your customers well, in particular, their needs and expectations, but also their desires and the positive emotions they’re looking for by doing business with you. You even need to pinpoint the stereotypes influencing the perception of your organization and its services which can hinder a memorable customer experience if they’re not broken. This exercise will provide you with clear indications on the customer experience they’re seeking and what they’re expecting (your service attributes) during their journey with you. It’s important to understand that in a B2B situation, the customer is a multifaceted individual, with needs, expectations, desires, emotions and stereotypes that can vary in the fine print. In this case, maintaining close communication at all levels in the organization to be able to deal with these differences will be a winning strategy. This exercise might seem obvious, but even today, few organizations bother to investigate beyond the simple needs and expectations of their clientele…

Assess how your organization performs in the creation of the customer experience your clientele is looking for and that you’re willing to offer.

On the basis of a known, relevant customer experience management model, assess whether your organization is truly focussed on the customer and identify performance gaps in your customer experience management.

On one hand, how is the customer culture within your organization? Does the organization’s leadership foster efforts in this regard? Have you defined and communicated your customer promise or service values to your staff? Are your employees committed to attaining a common goal, which is to better serve the customer?

On the other hand, are your customer experience delivery systems performing and consistent? First, do the employees have a good understanding of the customer experience to be delivered? Are they trained accordingly and do they exhibit the key behaviours of the customer promise? Second, do your work processes, procedures and tools enable your staff to go beyond the call of duty for your customers? Is the physical and virtual environment that you offer in line with the customer experience you’re trying to provide?

Lastly, do your efforts result in actual gains and create value for your organization? Managing the customer experience is not only for being nice to your customers; your organization must be able to reap the benefits. Do you have loyal customers? Would your customers recommend you? Will your brand image and the organization’s reputation be enhanced?

Take action

The issue is not having performance gaps, but rather failing to address them! You need to take action.

You need to implement a program to eliminate gaps in the current customer experience and what you want to offer while paying particular attention to revamping the organization’s customer culture and improving the performance of the three customer experience delivery systems, i.e., employees, organizational processes and systems and the physical and virtual environment. All must be aligned with the experience you want to offer customers. Mapping the customer journey is an excellent way of defining the customer experience in detail at each point of contact between your customers and yourself and to determine improvement methods that will later be used in a bold, yet realistic and sustainable action plan.

Success factors

The first success factor is being able to rely on management’s unconditional commitment. Managers must send a clear message about making the customer experience the corner stone of the business strategy and fostering success in order to motivate the staff to contribute. Improving the customer experience is done through inspirational management and leadership that will engage employees and motivate them to attain this common objective.

Lastly, as more than 70% of customer experience review projects fail at the implementation stage, sufficient efforts must be deployed at that point to ensure the necessary changes are implemented and that improvements last. The active supervision of developments and the use of tools such as scorecards including specific indicators can be useful for increasing the chances of success of a customer experience review project.

Have we convinced you? Are you already on the right path?

06 Dec 2016 | Written by :

Pierre Fortin is a partner at Raymond Chabot Grant Thornton. He is your expert in Management...

See the profileNext article

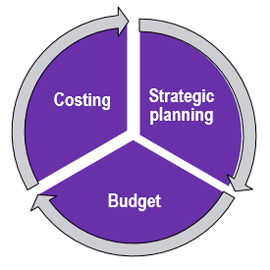

The best management accounting practices are very clear: the following three steps are a must if you want to turn your corporate strategy into concrete action while remaining true to your business context.

The best management accounting practices are very clear: the following three steps are a must if you want to turn your corporate strategy into concrete action while remaining true to your business context.

Step 1: Strategic Planning

This reflection must take account of certain concepts such as your corporate mission, vision, strengths, weaknesses, the opportunities your company needs to capitalize on and the threats it faces. Through this exercise, you can set your targets and turn them into strategic objectives and an action plan, which will guide you in making short-, mid- and long-term business decisions.

Since a strategic plan is an integral part of a business plan, it’s very likely your banker has already requested a copy to round out your file at the bank and become familiar with your initiatives and needs. Nevertheless, this plan isn’t set in stone; rather, it’s a process that evolves over time. Your strategic planning must reflect any significant changes in your market or event that alters your objectives and targets.

Step 2: The Budget

This phase involves quantifying the strategic initiatives and decisions established during your strategic planning. Your objectives and timelines are illustrated in a budget exercise wherein you estimate the resources needed to achieve your targets.

During the budget process, you will make decisions affecting several operational and financial aspects. For example:

- Sales volumes and product-specific production;

- Standard costs for raw materials and supplies;

- Energy costs;

- Labour costs;

- Operational performance;

- Product line,

- Product bills of materials;

- Capitalization initiatives;

- Etc.

This best practice is an ongoing process that requires a proactive approach. The budget is usually developed at the beginning of the year, and analysis meetings where discrepancies are explained must be a priority for those managing the budget.

Step 3: Costing

The strategic plan provided management with a direction, while the budget was used to evaluate the financial and human resources needed to achieve the objectives for the year. Now you need to ensure that the decisions made in the previous steps will enable the organization to deliver products and services at a cost and sale price that meet profitability objectives and satisfy market constraints.

It’s essential to calculate the cost per product and service. This step brings the decisions and assumptions made in the first two steps together in an operational whole. Various analyses, notably operating costs, costs per product or service, the distribution and profitability cost per client and product will help you measure whether you’re achieving your financial objectives. If objectives are not being achieved, costing will provide indications on which budget items or targets need to be adjusted.

We’ve noticed in our practice that few SMEs perform all three of these steps. Many of them only produce a budget since it’s often required by the bank or their business partners.

Failure to align the strategy, budget and costing often yields results that are below target. The following list of symptoms and scenarios may provide an indication that your strategy, budget and costing are misaligned:

- Sales are increasing but profits are declining;

- You’re making or losing money and don’t know why;

- You’re not able to assess the profitability of your products or services or that of your clients;

- Your business partners have little faith in your financial forecasting;

- Cost reduction initiatives are not bearing fruit despite the resources invested;

- Your business is evolving in a low-margin sector;

- You don’t produce a yearly budget or financial forecasts;

- Your costing hasn’t been reviewed in the past year or is unknown;

- The complexity of your products or services is not reflected in your rate setting;

- Your clients increasingly require custom products or services and this is not reflected in your rate setting.

Our team of experts can guide you in implementing tools and processes to achieve your objectives.

Please note that this article was co-written with Yann Vandevoorde, Analyst, Raymond Chabot Grant Thornton.

Next article

There are multiple reasons for selling a business. For some sellers, age, the approach of retirement, a sudden event such as illness, or simply the desire to do something else, lead them to consider selling their business.

In this context, regardless of the reasons for selling, the process is complex and ideally should be the object of a planned approach. This requires a major investment of time and effort to obtain the best possible price and favour the company’s sustainability.

1. Can I do it alone?

To carry out this process, you must consider several aspects involving specialists, such as business valuators, legal specialists, financiers, tax advisors and specialists in negotiation.

2. What is the value of the business?

Entrepreneurs usually know little about the value of their business. For many of them, the selling price of the business is based on the amount of money they want for their retirement. In this regard, a business valuation should be obtained before engaging in a selling process, so that a good basis for negotiation is established. Not only must the company’s assets be appraised, but its fair market value must be established.

3. What about taxes?

Tax planning related to the transaction is also essential. It needs to be planned methodically, because a shareholder who sells his company’s shares (and not the assets) has the right to a capital gains exemption of up to $800,000, if he meets certain very specific criteria. For entrepreneurs who want to sell their business so they can constitute their retirement fund, this tax benefit becomes especially important.

4. Have you established a communications and marketing strategy?

In the process of selling a business, communication is essential, both with the buyer and with the team in place within the business and the key employees. Is there internal interest, or a risk of losing one or more key employees?

5. Can you control your emotions?

Entrepreneurs often have invested a large part of their lives in the business. They are involved both in human and financial terms. It is therefore completely normal to be emotionally involved when you consider divesting your life’s work.

But there is no place for emotionalism in the process of selling a business. For this reason, support to the seller by a person who has no interest in the business is very beneficial in such transactions.

Just as entrepreneurs are experts in their industry, entrepreneurs involved in a selling process should call on the best resources at their disposal. Ultimately, the wealth he needs to ensure his retirement is in question.

31 Mar 2015 | Written by :

Gilles Fortin is your expert in corporate finance for the Québec office. Contact him today!

See the profile