Share

Published on April 30, 2018

It is no secret that the crisis caused by COVID-19 has significant financial repercussions for companies and represents a real headache for managers.

Use Industry 4.0 technology to boost operational and financial data cross-referencing to determine production costs more quickly and be more competitive.

Production cost and measuring processes

Production costing could be described as cross-referencing operational and financial information that are often in separate systems together into a common structure.

The purpose of operational data is to measure a business’s various processes (speed, quality, satisfaction, etc.) while financial data indicate the cost of resources needed to operate these processes. The two data help determine the cost of the manufacturing process, distribution, sales, client experience, etc.

Individually, operating and financial data do not provide the same informational value or foster quick and efficient decision-making.

The operational data challenge for production costs

The level of corporate informational maturity varies greatly, and data collection methods range from notes on paper to integrated management systems (ERP), and the ubiquitous Excel spreadsheet. Until recently, we were rarely able to access structured, quality data. Instead, data compilation, validation and transformation exercises were required to obtain accurate data that could be used in costing. Today, organizations are facing two major revolutions:

- Easy access to digitization

There has been an abundant supply of products and services in this field in Quebec for several years now, making it possible to quickly obtain accurate, structured operational data; - The enhancement of existing data

Many companies have an unsuspected information asset in their hands. They accumulate data in ERPs, machine tools or other systems without exploiting them.

With artificial intelligence et advanced analytical techniques, it is now possible to enhance these data and gain an important competitive advantage.

With the data acquired by digitizing processes or using existing data, the company can determine the production cost more quickly and often more accurately. It is also possible to exploit the benefits of costing and to analyse profitability by product, customer, order, etc., based on available information and the company’s objectives.

A practical example

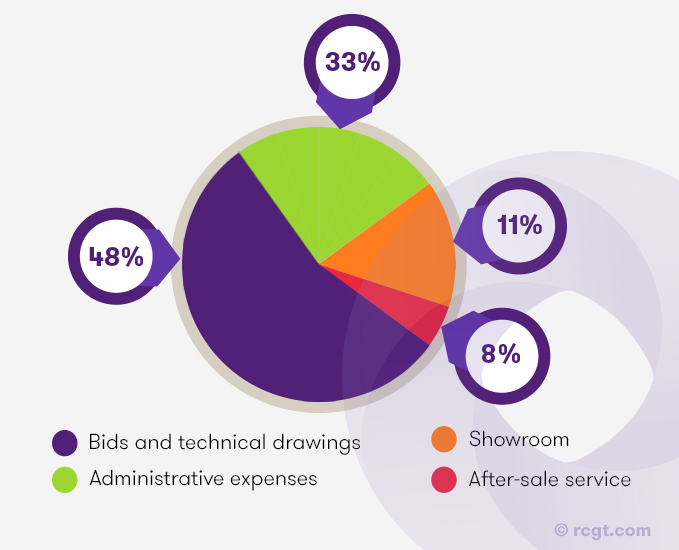

A summary analysis provided the following information: 47% of the costs incurred are operating costs, 53% are selling and administrative costs. An analysis of the 53% production costs revealed that they consist of the following services:

Findings:

To support its distributors, for several years the company has been hiring more resources to prepare bids and technical drawings with no corresponding rise in sales.

Exploiting data to understanding how costs behave

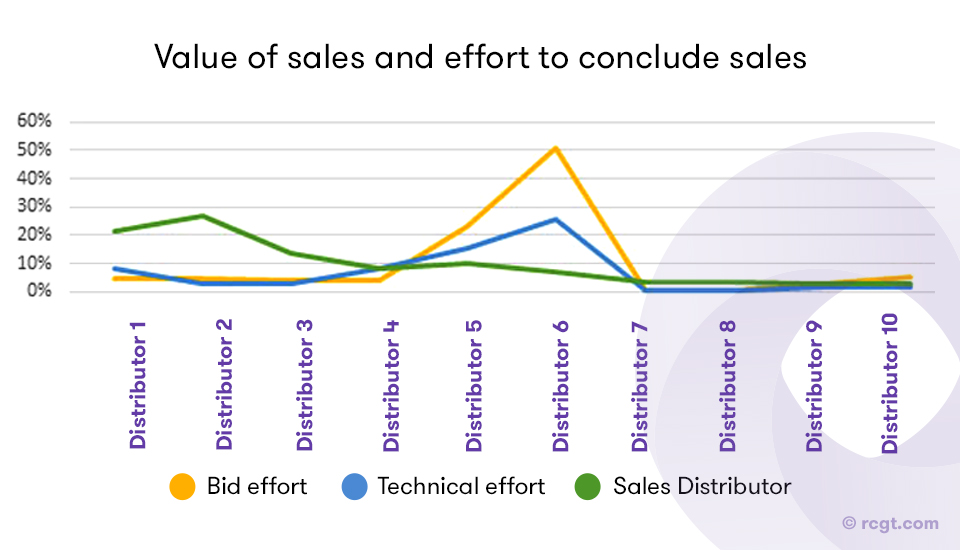

By analysing six variables over time and adding qualitative data, it was possible to define measurements that characterized each of the distributors:

- Measurement 1: Success rate (sales $/bid $);

- Measurement 2: Bid cost per distributor;

- Measurement 3: Technical drawing cost per distributor;

- Measurement 4: Sales per distributor.

The above graph indicates that distributors 1 and 2 account for less than 10% of the bids and technical drawing departments’ efforts and 50% of sales. On the other hand, distributor 6 accounts for 50% of the bid department’s efforts and 25% of the technical drawings department’s effort.

Return on investment

On the basis of this analysis, the company drew up a clear portrait of each distributor’s contribution. Using this information and an analysis of the six underlying variables, the company:

- Discussed potential improvements with distributors;

- Targeted training efforts;

- Identified the efficient distributors’ good practices and passed them on to the others;

- Introduced fees for certain services;

- Eventually, dropped the distributors that did not show any improvements, despite the measures taken.

Whether data come from an ERP, artificial intelligence or elsewhere, if they are not used, there is no return on investment.

Our consultants are available to help you initiate or continue your 4.0 transformation and support your projects, from the smallest to the most ambitious. Go for it!